Introduction

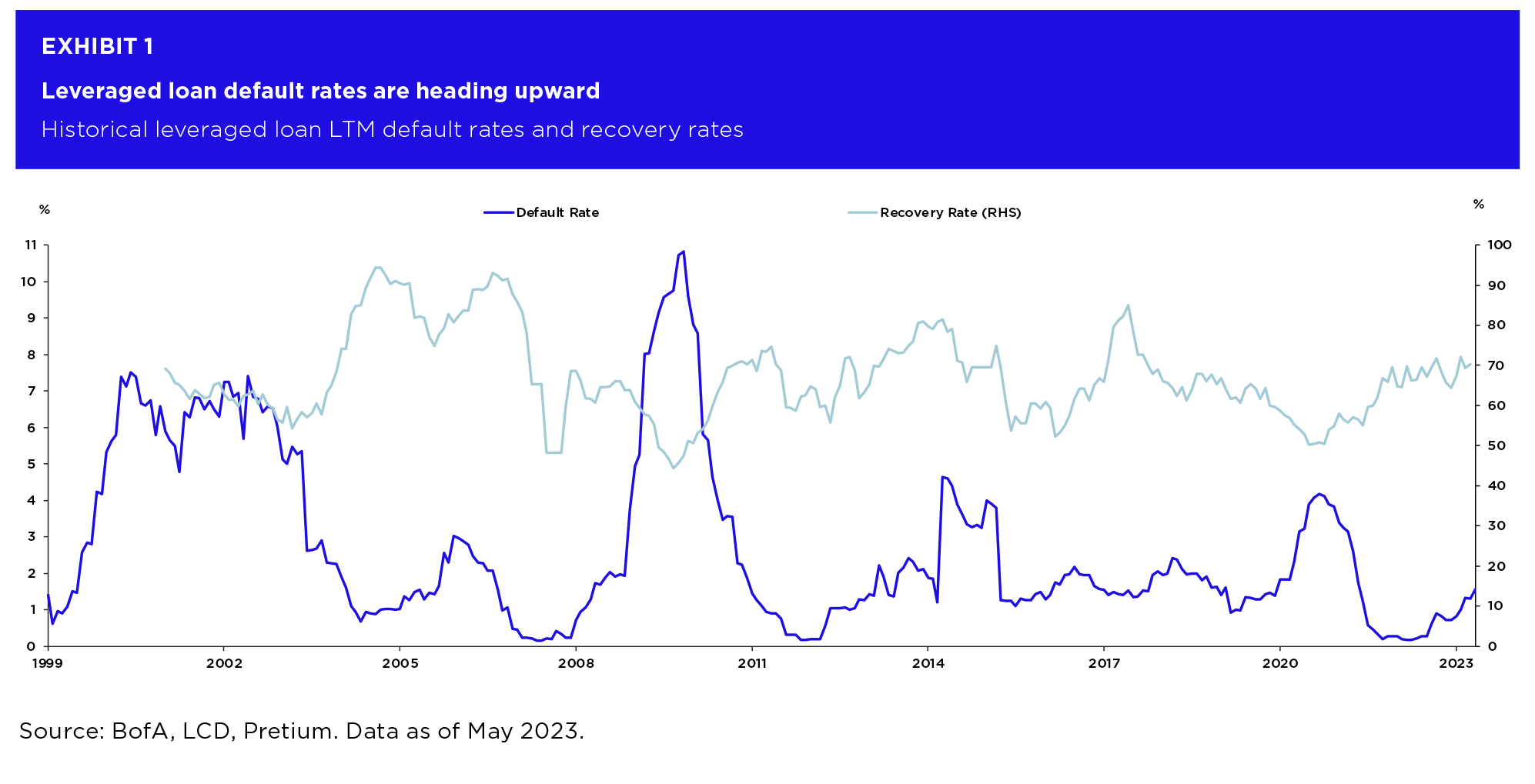

The junior portion of the CLO capital structure has seen solid performance so far in 2023. Over the course of the past several months, Pretium has highlighted this outperformance and made the argument that CLO mezzanine securities were undervalued relative to HY single-name credit, supporting this latter point by comparing the currently wide CLO BB spreads to the historical spread relationship the two asset classes have traditionally maintained. Given the uncertainty surrounding where the economy and the Federal Reserve may go from here, we have received inquiry from our investor base as to whether or not we view this outperformance as sustainable. In summary, we believe it is. Pretium believes that current CLO mezzanine and equity pricing reflects worst-case assumptions related to forward defaults and recoveries. While Pretium expects loan default rates to rise and recovery rates to remain depressed, we believe that current CLO spread and yield levels more than compensate for the fundamental strain that credit markets have already begun to realize and are likely to continue to experience over the coming quarters (Exhibit 1 below).

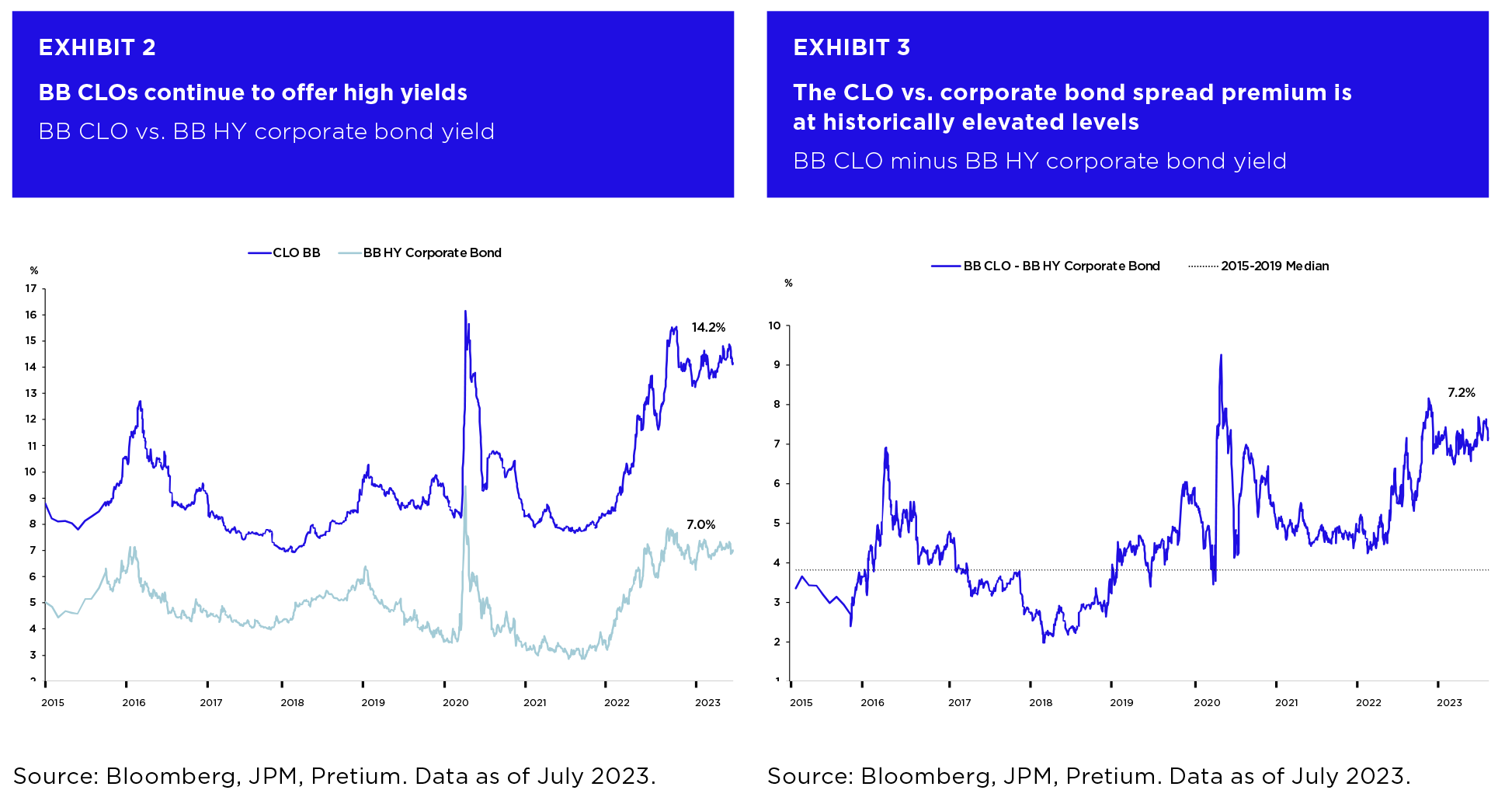

CLO BBs and CLO equity provided +8.6% and +7.6%, respectively, in (non-annualized) total returns over the first six months of the year vs. just +4.8% for HY corporate bonds1. Pretium believes this strong YTD performance for CLO instruments is sustainable across a variety of possible forward market outcomes. The market environment in the first half of 2023 reflected only muted spread changes and close to flat point-to-point long-term interest rate moves. Thus, the strong 23H1 CLO results for that period reflect what we see as only slightly above average expected returns for a sector which entered the year offering particularly generous spreads and yields.

BB CLOs began 2023 with average yields of approximately 14%, reflecting SOFR margins at the time of over 900 basis points2. The strong total return for BB CLOs over the first half of 2023 largely reflected interest carry, as opposed to mark-to-market price gains which might have been harder to replicate in the future. By contrast, BB corporate bonds have yields-to-maturity of just 7%, with correspondingly smaller scope for carry returns (Exhibits 2-3 below).

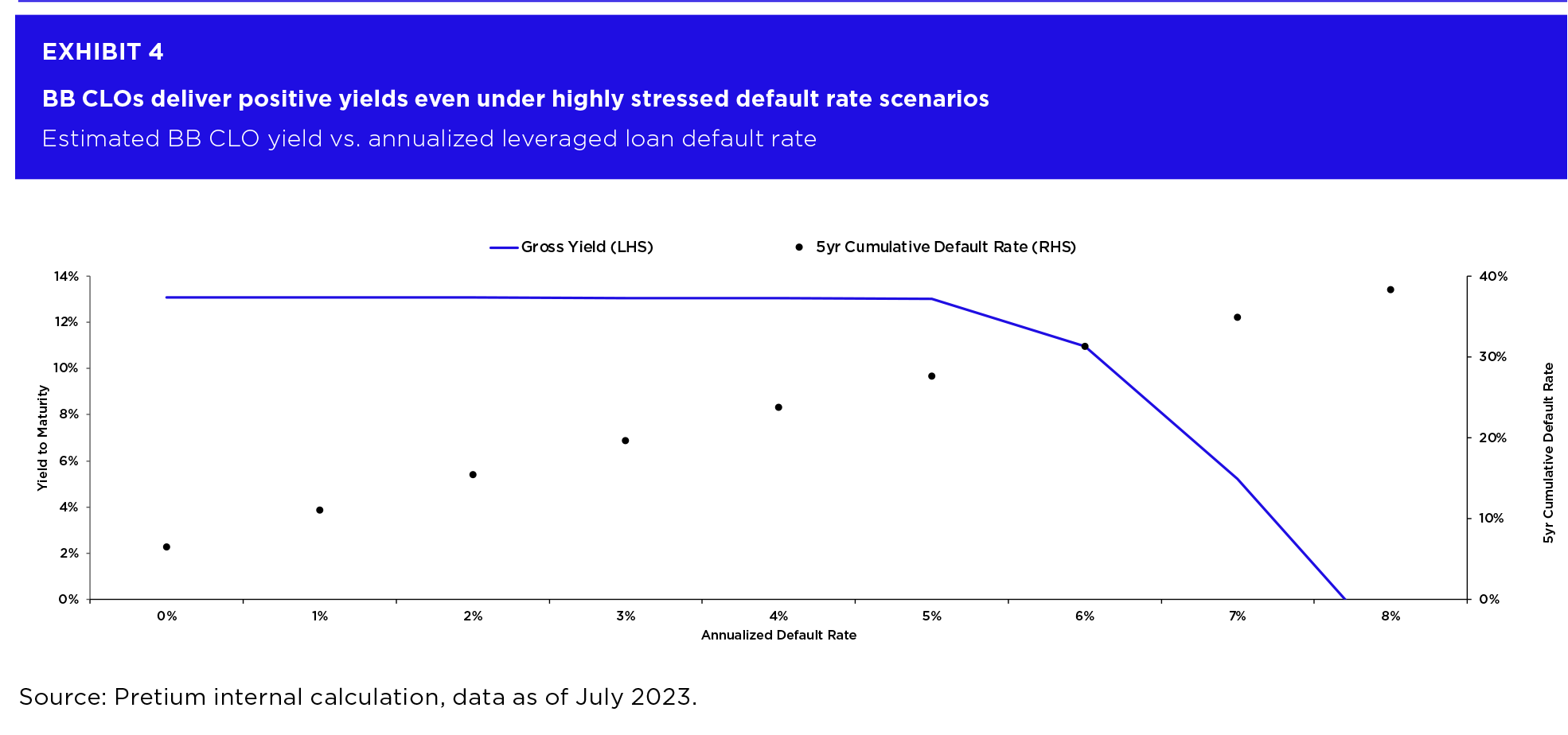

To assess the sustainability of CLO outperformance going forward in greater detail, we review expected returns for CLOs across a range of possible future interest rate and macro-economic scenarios. Our analysis suggests that mezzanine CLOs should outperform generic HY corporate bonds over a short-term (e.g., 1-year) horizon across most scenarios, with an even higher probability of outperformance over a hold-to-maturity horizon. Long-term expected returns for CLO BBs remain elevated under adverse scenarios at current pricing levels due to the fact that the investments benefit from significant structural protections which allow for full principal repayment under all but the most extreme default and recovery rate assumptions (Exhibit 4 below).

While CLO BBs can provide long-horizon downside protection in deep recession scenarios, CLO equity can complement the profile of CLO debt by offering a return distribution with significant upside potential in scenarios involving only mild recession or recovery. Combined, a portfolio which incorporates both CLO equity and CLO debt securities produces a highly attractive distribution of returns across a range of potential future economic outcomes.

Interest Rate Scenarios and Their Impacts on CLO Returns

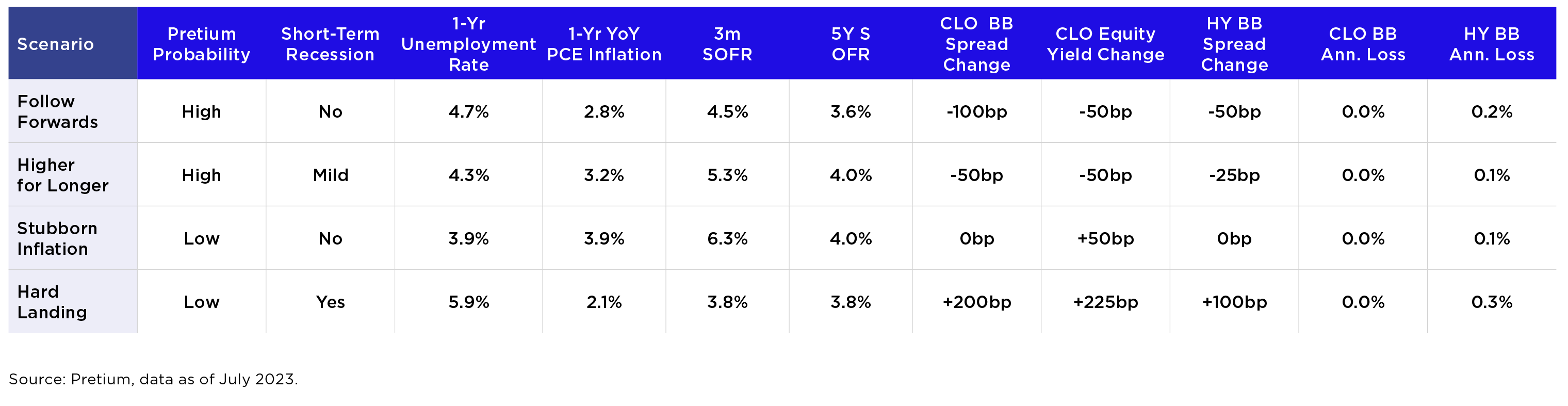

The scenarios we include in our analysis are:

- 1. Follow Forwards (high probability). Current interest rate curve plays out in line with current forwards, inflation continues to move down from current spot levels but remains above 2% target, unemployment ticks up modestly and corporate earnings stay flat or see a muted pullback: a soft landing scenario in which credit will outperform vs. current pricing and realized defaults are slightly below the market baseline forecast.

- 2. Higher for Longer (high probability). Interest rates stay higher for longer, remaining close to current spot levels, inflation comes down slightly but remains elevated, unemployment ticks up and corporate earnings stay flat or see a muted pullback: a soft landing scenario in which credit will marginally outperform vs. current pricing and defaults are in-line with the market baseline forecast.

- 3. Stubborn Inflation (low probability). The Federal Reserve hikes rates over the next twelve months in response to stubborn inflation and strong corporate earnings, inflation remains unchanged vs.current spot levels and unemployment remains low: a short term bullish market for credit with default rates lower than forecast due to strong corporate earnings.

- 4. Hard Landing (low probability). Material economic weakness emerges in the second half of 2023, inflation trails lower towards target and unemployment becomes elevated: a hard landing scenario for the economy and credit with short term and long term default rates above baseline forecasts and pulled forward.

Further detailed assumptions regarding these scenarios, including the assumed unemployment rate, inflation rate and short and longer term interest rates, are provided in Appendix A.

The calculations of expected CLO and corporate bond returns under the alternative scenarios incorporate both projected coupon income (e.g., with lower income for floating rate CLO instruments in falling rate scenarios) combined with, over the short horizon, expected mark-to-market price changes, and, over the longer term, potential realized credit losses.

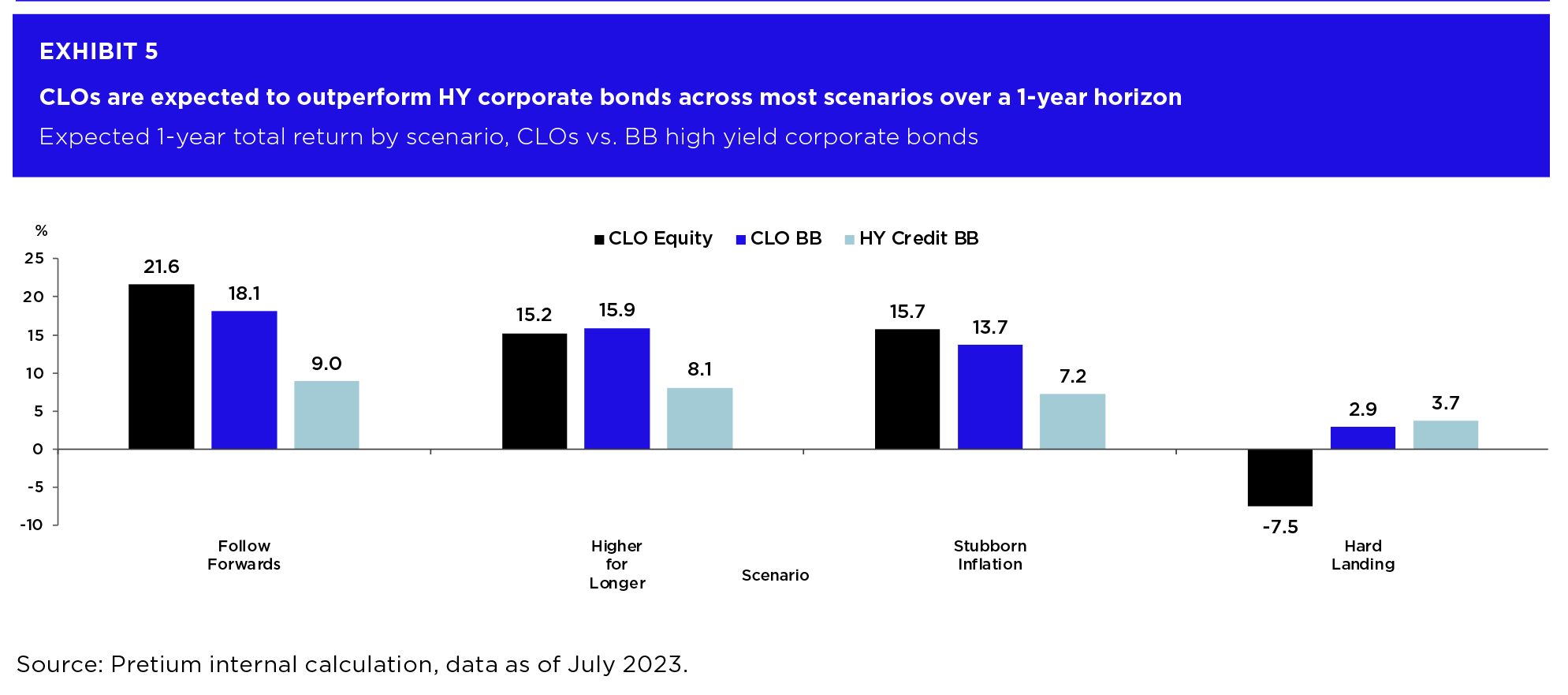

Short-Term Outlook

Exhibit 5 below shows the estimated scenario returns over a one-year horizon holding period. In scenarios 1 to 3 the returns for BB CLOs are projected to significantly exceed those for BB corporate bonds. This outperformance is driven by higher coupon income for CLOs. In effect, the projected outperformance of CLOs in these scenarios mirrors the recent historical outperformance of CLOs vs. HY bonds, which has also been largely driven by superior carry for the CLOs.

For scenario 4, a Hard Landing, CLO BBs are projected to deliver lower returns than fixed rate HY bonds. This modeled underperformance is a consequence of an expected decline in CLO floating rate coupons as the Federal Reserve cuts interest rates in response to an economic contraction, combined with an assumption that generic fixed rate bond spreads widen less sharply than CLO BB spreads into the contraction.

The short-term CLO equity performance estimates shown in Exhibit 5 are calculated from the cash-on-cash equity yields expected in these scenarios combined with expected instrument price changes; the price change estimates, in turn are estimated based on the historical relationships between CLO equity and HY bond prices across different market environments. In scenarios 1 to 3, CLO equity is projected to significantly outperform BB corporate bonds as high current carry is offset by only marginal changes in cash flow discount yields. Near-term changes to discount rates remain range-bound as default expectations over the first year are primarily constructed from credits that are already identified as candidates for default as a function of their current trading price. In scenario 4, CLO equity is projected to underperform as the pull-forward of defaults in credits that are currently trading above $90 is likely to result in a downward revision to forward cashflow projections combined with an increase in market yields used to discount the cashflows.

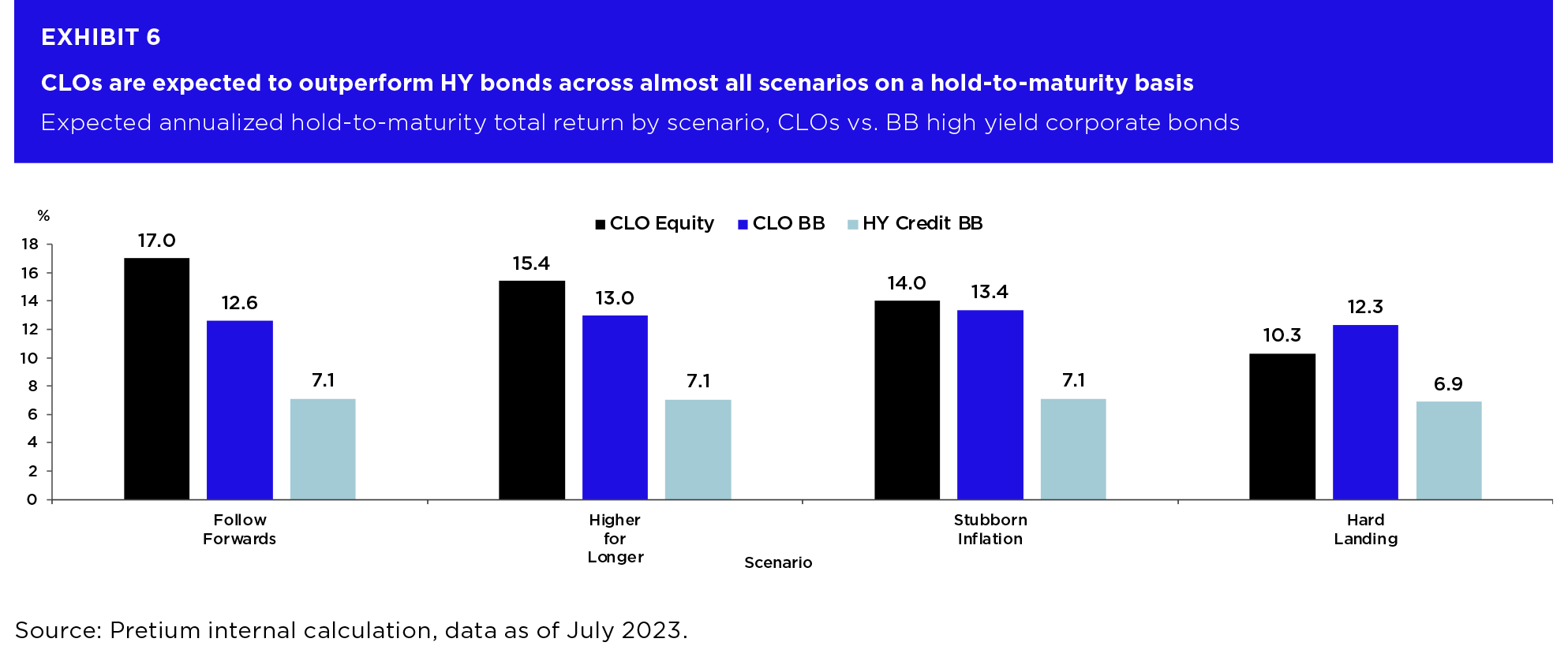

Hold-to-Maturity Outlook

Exhibit 6 shows the expected hold-to-maturity returns for the different asset classes across scenarios. Here, CLO BBs are projected to outperform HY BB bonds across all the scenarios, including the Hard Landing. Historically, only a small percentage of BB CLOs have ever experienced principal losses, including during the global financial crisis period, due largely to the structural protections from which the bonds benefit3. Accordingly, we project no CLO BB losses under the four scenarios considered. Generic HY corporate bonds lack these structural protections and hence, are projected to experience small but non-zero performance drags due to defaults, which are modeled here as ranging from a 0.1% annualized yield degradation in the more benign scenarios to a 0.3% yield impairment in the Hard Landing scenario. Most of the projected BB CLO vs. BB corporate bond outperformance though, comes not from differences in credit loss assumptions but rather, from the substantially wider spreads CLO BBs currently contain, which helps generate much stronger carry income over the lives of the respective bonds.

While CLO debt is seen in Exhibit 6 to provide high prospective yields and significant long-horizon downside protection, CLO equity offers a return distribution with significant upside potential in scenarios involving milder recession or recovery. For example, in the Follow Forwards scenario, CLO equity would be expected to deliver a 17% annualized return. Combined, a portfolio incorporating CLO equity and CLO BB securities can produce a risk-return profile superior to those available in public equity or single-name HY credit markets.

The hold-to-maturity CLO equity performance estimates in Exhibit 6 are based on IRR calculations which project CLO equity cash flows under the alternative scenarios. The modeled CLO equity held-to-maturity return is lowest in the Hard Landing scenario, in which loan default rates are assumed to be relatively elevated and CLO equity cash flows are consequently reduced. Lower interest rates in this scenario also put downward pressure on CLO equity cash flows in this adverse scenario. Even in the Hard Landing scenario however, we project a portfolio of CLO equity securities to ultimately deliver low double-digit IRRs given the currently favorable pricing of these instruments

Summary

Our analyses suggest that the strong total returns delivered by CLO mezzanine debt and equity securities in the first half of 2023 are sustainable going forward given current pricing. An analysis of the projected returns for CLOs vs. fixed rate HY corporate bonds suggests that CLOs should outperform over a 1-year horizon across most economic scenarios, with outperformance even more probable over longer holding periods. Pretium believes the attractive relative value provided by a portfolio of CLO equity and CLO BBs clearly indicates that CLOs should be an integral component for every allocator looking to optimize their corporate credit exposure in this environment.

Appendix A — Economic scenario assumptions