Collateralized loan obligations are investment vehicles that securitize a diversified portfolio of senior secured corporate loans – sometimes referred to as leveraged loans – and then distribute the loan portfolio’s cashflows to a range of end investors. The equity tranche of a CLO transaction is entitled to all of the principal and interest payments made by the underlying loan portfolio, net of interest and principal payments distributed to the CLO debt securities senior to the equity tranche. Thus, a key attribute of CLO equity, as it relates to the priority of payments received, is that CLO equity receives regular periodic payments representing the excess interest generated by the difference between the loan portfolio income and the CLO debt security cost, on a current basis.

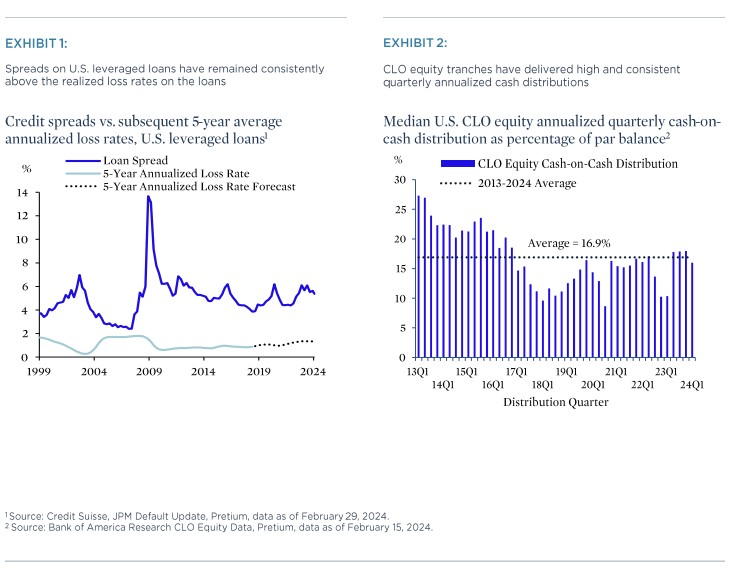

The senior secured, high-yield corporate loans that back CLO transactions have historically been attractive assets to own, as their spreads have remained well above the loans’ realized credit losses. Exhibit 1 below shows that leveraged loan spreads have averaged 5% (500bp) over the past 25 years while leveraged loan losses have averaged only 1% (100bp) over the same period, highlighting the potential for the loans to generate positive long-run excess returns.

CLO equity is, in turn, a particularly unique format through which to gain exposure to high-yield corporate loans. The CLO structure – as shown, e.g., in the Appendix of this report – provides non-recourse, non-mark-to-market term leverage, which enhances the baseline yields of the loans themselves, without incurring risks of margin calls which may occur when using more traditional forms of leverage such as repo financing. Additional positive features of the CLO equity asset class include multiple embedded options, such as the option to refinance senior CLO debt when conditions are favorable and the option to actively manage the underlying CLO loan portfolio through asset sales and purchases, and limited interest rate risk exposure due to the floating-rate nature of the CLO assets and liabilities.

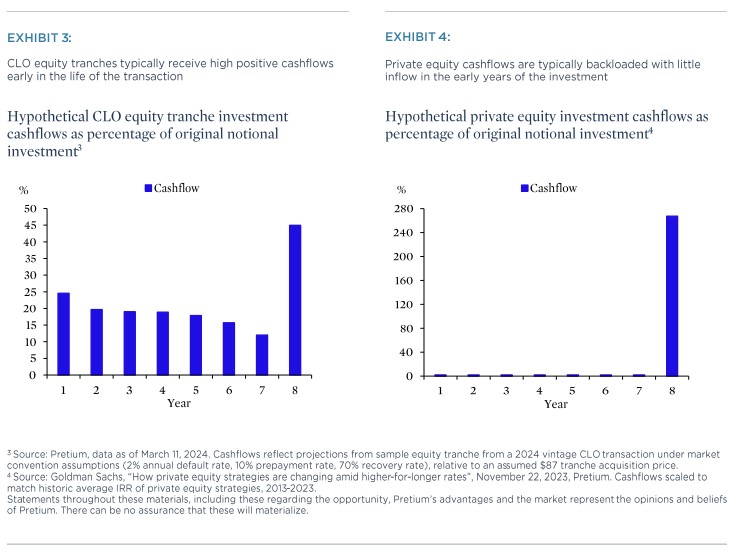

The beneficial features of CLO equity listed above have helped the sector to generate high and consistent quarterly cashflow distributions over time. Exhibit 2 above shows that CLO equity cash-on-cash returns have historically averaged 16.9%, annualized, when expressed as a percentage of the equity tranche par value; when these cash distributions are expressed as a percentage of acquisition value (purchase price), they further increase, as new issue equity is typically issued at a discount to par and seasoned secondary market equity often trades at a significant discount to par. As an example, if the equity tranches are acquired in the secondary market at a $90 price, as is often feasible, then the average annual cash-on-cash return as a percentage of purchase price becomes 18.5%; if the tranche acquisition price is $75, then the cash-on-cash return becomes 22.5% annualized.

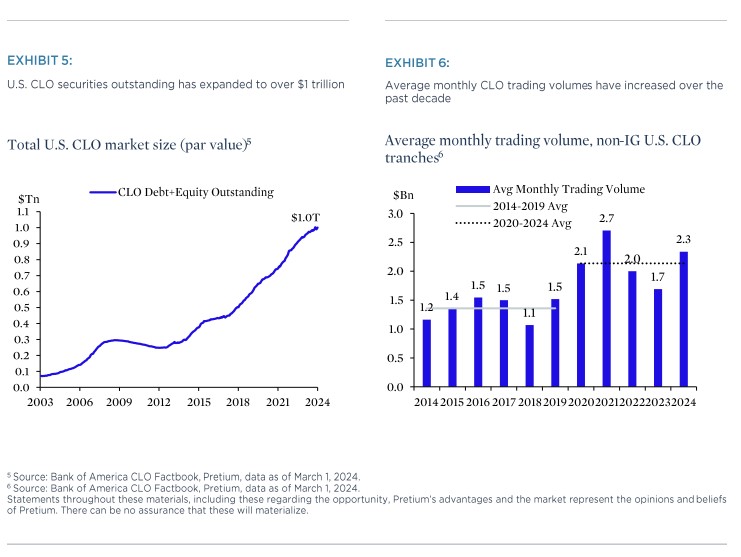

Notably, the distributions to CLO equity usually begin on the first payment date and continue on a quarterly basis over the life of the investment, as is shown in Exhibit 3 for a hypothetical equity tranche. The resulting cash flow profile compares favorably to traditional private equity investments, which commonly exhibit a “J-curve” profile in which the investment delivers negative returns/no cash flow in the initial years of the transaction, hopefully to be offset by positive returns and return of capital in later years as the investment matures, as per Exhibit 4.

Growth of U.S. CLO market allows equity investors to allocate selectively

The U.S. CLO asset class has expanded to over $1 trillion of securities outstanding, from less than $500 billion in 2017, making CLOs now the largest securitized credit asset class in the U.S. (Exhibit 5). The growth of the CLO market is in large part a consequence of the sector’s historic success in delivering solid returns to investors through multiple cycles including the global financial crisis and COVID-19, while providing a dependable source of financing to a large and growing segment of corporate borrowers. The growth of the CLO market has led to improved trading liquidity for the asset class (e.g., per Exhibit 6) and makes it possible for active CLO equity investors to focus upon specific sub-segments of the market in order to target particularly compelling risk-reward profiles while still remaining discriminating in terms of security selection. For example, as market volatility and price dislocation increased in 2022 and 2023, Pretium adjusted its allocation strategy by overweighting secondary vs. primary market CLO equity positions and by overweighting CLO equity tranches backed by relatively defensive, lower risk loan portfolios. To the extent price dislocation moderates in 2024 and financing markets continue to become more accommodative, Pretium would expect to become more active in new issue markets again in order to lock in favorable debt terms which would benefit new issue CLO equity.

Conclusion: CLO equity is an attractive alternative for asset allocators looking to diversify their private credit exposure

CLO equity tranches have the potential to generate double digit returns over the long term while generating high current cash flow. The sector offers insulation from an uncertain future for interest rates and the large market footprint allows active investors to generate excess returns through tactical asset selection. Pretium believes the risk/reward characteristics of CLO equity to be a complementary component to any private credit allocation strategy today.

Appendix: Sample CLO Transaction Structure

CLO transaction structures distribute the principal plus interest cashflows from a pool of ~200 senior secured corporate loans to a range of equity and debt tranches.

Jerry Ouderkirk – Senior Managing Director, Head of Structured Credit

Jerry Ouderkirk is a Senior Managing Director and Head of Structured Credit at Pretium, where he has overall responsibility for the Firm’s corporate credit platform. In addition to overseeing and expanding the Firm’s CLO platform, Mr. Ouderkirk is building out numerous investing businesses across structured credit including Structured Corporate Credit.

Mr. Ouderkirk joined Pretium in 2017 with 20 years of experience building and committing capital around structured credit products and platforms. Prior to joining Pretium, Mr. Ouderkirk was a Partner at Goldman Sachs, where he started the Institutional Lending Group for Goldman Sachs Bank USA which oversaw the Firm’s discretionary lending and investing in the bank. He previously served as Global Co-Head of Structured Credit Trading, where he oversaw multiple capital committing businesses and started Goldman’s CLO Trading business, which he ran for more than 12 years.

Mr. Ouderkirk is a member of the Firm’s Executive Committee. He received a BA with honors in English and Economics from Colgate University. Mr. Ouderkirk serves on the Board of CitySquash in New York.